A bond is essentially a loan that you, as an investor, give to a government, corporation, or agency. In return, the issuer agrees to pay you back the full amount (called the face value) on a specific future date. Until then, you receive regular interest payments, known as coupons.

Unlike stocks, bonds do not offer any ownership in the company or organization. If you own a stock, you become a partial owner and share in profits and losses. If you own a bond, you’re a creditor—your main concern is getting your money back with interest, not whether the company grows or fails.

Because of this structure, bonds are often seen as more stable and predictable than stocks, making them a popular choice for investors looking to reduce risk or receive steady income over time.

Key Features That Define Every Bond

Before trading bonds, it’s important to understand the key components that make up each one. The face value is the amount you’ll be repaid when the bond matures—this is typically set at $1,000, but it can vary. The maturity date is the deadline by which the issuer must return the full amount. Between the issue date and maturity, you’ll earn interest based on a set coupon rate, which is usually expressed as a percentage of the face value.

Interest payments are made on what’s called the coupon dates, which are often semiannual. The issue price—the price at which the bond was originally sold—can differ from the face value depending on interest rate conditions and investor demand.

These characteristics help investors estimate how much income they’ll earn and how risky a particular bond might be:

- Face Value (Par Value): This is the amount you’ll be repaid when the bond matures. Most commonly, bonds have a face value of $1,000.

- Coupon Rate: This is the interest rate the bond pays annually, expressed as a percentage of the face value. A 5% coupon on a $1,000 bond pays $50 a year.

- Maturity Date: The date when the issuer must repay the face value to the bondholder. Bonds can mature in months, years, or even decades.

- Issue Price: The initial sale price of the bond, which may be above or below face value, depending on market interest rates at the time of issuance.

Understanding these basics helps you estimate how much income you’ll earn and assess how sensitive a bond might be to market changes.

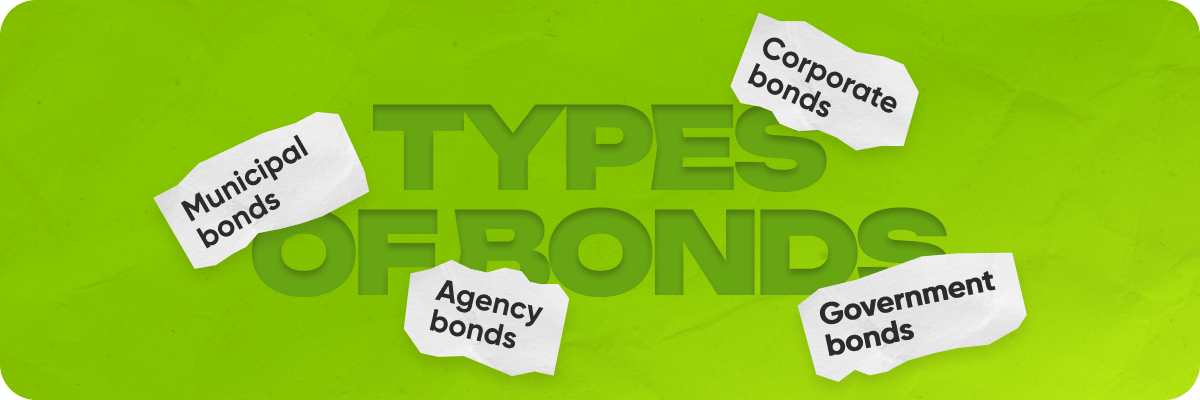

Types of Bonds and Who Issues Them

Bonds come in several types, largely based on who issues them. Government bonds, for example, are issued by national governments and are considered among the safest investments. U.S. Treasury bonds are a classic example. On the other hand, corporate bonds are issued by companies that need funding but prefer not to borrow from banks. These tend to offer higher returns but carry greater risk, especially if the issuing company faces financial trouble.

Municipal bonds are issued by local governments like cities or states. A key advantage of these is that their interest income is often exempt from taxes. Lastly, agency bonds are issued by government-affiliated institutions. These fall somewhere between government and corporate bonds in terms of risk and return.

Each type plays a different role in an investment strategy, depending on your risk tolerance and income goals.

Holding vs. Trading Bonds: Two Different Approaches

When you hold a bond, you simply collect interest over time and get your money back when the bond matures. This is the more conservative approach and is ideal for those who want predictable income with minimal effort.

Trading bonds, however, involves buying and selling them on the secondary market before they reach maturity. Bond prices fluctuate based on market interest rates, credit ratings, and other factors. If interest rates fall after you buy a bond, its market value usually increases, giving you a chance to sell it at a profit. This strategy requires more knowledge and market awareness but can lead to additional gains.

For example, a professional trader might buy a long-term corporate bond at a discount when a company’s credit rating is under review, then sell it at a premium once the rating improves. This kind of trading isn’t about luck—it’s about timing, analysis, and understanding the broader economic picture.

There are two main ways to approach bond investing: holding bonds until maturity or actively trading them.

- Holding to Maturity: This is a conservative, income-focused strategy. You buy a bond, collect fixed interest payments over time, and receive the face value when the bond matures. It’s ideal for investors seeking stability and predictable returns.

- Trading Bonds: This involves buying and selling bonds on the secondary market. Prices fluctuate with interest rates, inflation expectations, and credit risk. If market rates fall after you purchase a bond, its market value can rise—allowing you to sell at a profit before maturity.

For example, a professional trader might buy a long-term corporate bond at a discount when a company’s credit rating is under review, then sell it at a premium once the rating improves. This kind of trading requires good timing, analysis, and awareness of broader economic trends.

Practical Strategies for Beginners

For newcomers, it’s usually best to start simple. A popular strategy is the bond ladder. This involves buying several bonds that mature at different times. As each one matures, you reinvest the money into a new bond. This spreads out your risk and ensures you always have some cash becoming available.

Another strategy, the barbell, splits your investments between short-term and long-term bonds. The short-term portion gives you flexibility, while the long-term portion locks in higher interest rates.

If you’re just starting out, consider these beginner-friendly tips:

- Start with Government Bonds: These are the safest and least volatile. They’re a good entry point for learning how bond markets work.

- Use a Bond Ladder Strategy: This helps manage interest rate risk by spacing out maturity dates, giving you flexibility to reinvest in changing market conditions.

- Stick with Investment-Grade Bonds: Bonds rated BBB or higher are considered less likely to default. Lower-rated “junk bonds” may pay more but carry higher risk.

These approaches don’t require constant monitoring and are a good way to build experience without unnecessary complexity.

Tools You’ll Need to Get Started

To begin trading bonds, you’ll need a brokerage account that supports bond investing. Many platforms now offer access to both new bond issues and the secondary market. A bond screener helps you filter opportunities based on factors like interest rate, maturity, and credit rating.

Here are a few essential tools and resources to guide your journey:

- Bond Screeners: These help you find bonds that match your desired credit rating, yield, and maturity range.

- Economic Calendars: Central bank meetings, inflation data, and jobs reports can impact bond prices. Staying updated helps you trade with context.

- Credit Rating Reports: Provided by agencies like Moody’s and S&P, these offer insights into the financial health of issuers. Higher-rated bonds typically offer lower yields but are safer.

Using these tools ensures you’re making informed decisions based on real data, not just guesswork.

How Professionals Trade Bonds in Real Markets

Institutional traders and fund managers trade bonds not only for income but to manage portfolio risk. One common tactic is watching credit spreads, which compare the yield of a corporate bond to a government bond. A widening spread signals rising perceived risk. Professionals also use derivatives like interest rate futures or credit default swaps to hedge their positions or speculate on interest movements.

While these advanced methods are out of reach for most beginners, understanding that bond markets are active, dynamic, and influenced by real-world events gives you a broader view of how bonds work beyond the basic “buy and hold” method.

Final Thoughts

Bonds might seem complex at first glance, but they become much more approachable once you understand their structure and role in the financial markets. They are a critical part of many investment portfolios—offering stability, income, and opportunities for smart trading.

As a beginner, focus on mastering the fundamentals: what bonds are, how interest works, and how different market factors affect their value. Start with safe instruments like government or investment-grade corporate bonds, and explore more complex strategies once you build confidence.

Trading bonds is about steady thinking, planning ahead, and using the right tools. It’s not just for big institutions—anyone with curiosity and patience can learn to trade bonds effectively.